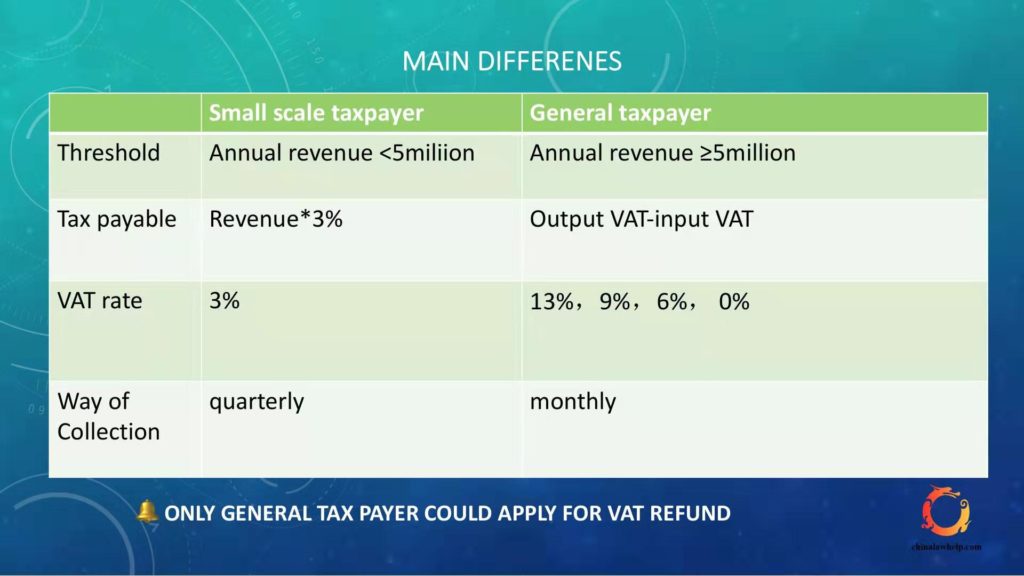

All companies in China have to pay value-added tax ( “VAT” ) based on their taxable revenue. According to related taxation laws of China, VAT taxpayers are categorized into general taxpayers and small-scale taxpayers based on their annual taxable sales.

Taxpayers with annual revenue exceeding the ceiling set for small scale taxpayers must apply for general taxpayer status. The current ceiling for all companies is 5 million RMB a year.

What’s the difference between these two kinds of taxpayers and can we choose what kind of taxpayer to be?

1. What are the differences?

Small scale taxpayers are subject to lower uniform VAT rate of 3 percent, as compared to rates ranging from 0 to 13 percent for general taxpayers ( please check our previous post for more info: Corporate Burdens-Reduced Further ), but they cannot credit input VAT from output VAT, nor are they entitled to VAT export exemptions and refunds.

Small scale taxpayers pay tax quarterly. Small scale taxpayers can only issue ordinary invoices , they have to ask the tax agency to issue VAT special invoices if necessary(unless they are in certain industries)

However, small scale taxpayers are entitled to the tax cut policy from 2019-2022 ( please the relevant post for more info: Tax Reduction in China-More Details).

For general tax payers, there are different VAT rates for different industries,which are:

1) 13%

for companies selling or importing goods (except for some special listed goods) or providing processing or repair services;

2) 9%

for company selling special products or real estate or providing construction, transport, postal or basic telecommunications services;

3) 6%

for companies providing modern services such as financial or value-added telecommunications services, IT and Cultural Creative Services and other life services.

Additionally, general taxpayers can credit input VAT from output VAT, and they are entitled to VAT export exemptions and refunds.

General tax payers have to pay tax monthly and they can choose to issue ordinary invoices or VAT special invoices.

You can check the following charter for an better understanding:

2. Can we choose?

Generally speaking, if any company’s annual taxable revenue reaches the ceiling of 5million RMB, then it will be treated as a general tax payer. However, companies with an annual revenue below the ceiling and those who have recently established their business, can voluntarily apply to be general taxpayer as long as they are capable of setting up legitimate, valid, and accurate bookkeeping.

3. How to choose?

So, should your company be a general tax payer or a small scale tax payer? From what we described above , it’s not hard to tell what the pros or cons are for general tax payers or small-scale taxpayers.

If your clients need VAT special invoices and your suppliers or service providers can provide you with VAT special invoices, it’s better to be an general tax payer.

If your clients don’t need VAT special invoices as much, and your suppliers or service providers are reluctant to provide VAT special invoices, then you should choose to be a small scale tax payer.

If you export a lot and want to claim a VAT refund, then you would rather be a general tax payer. Of course, the prerequisite is that you should make sure your company has established a sound accounting system.

Is it clearer now?

Useful link: